Chapter 3

Bodily Injury

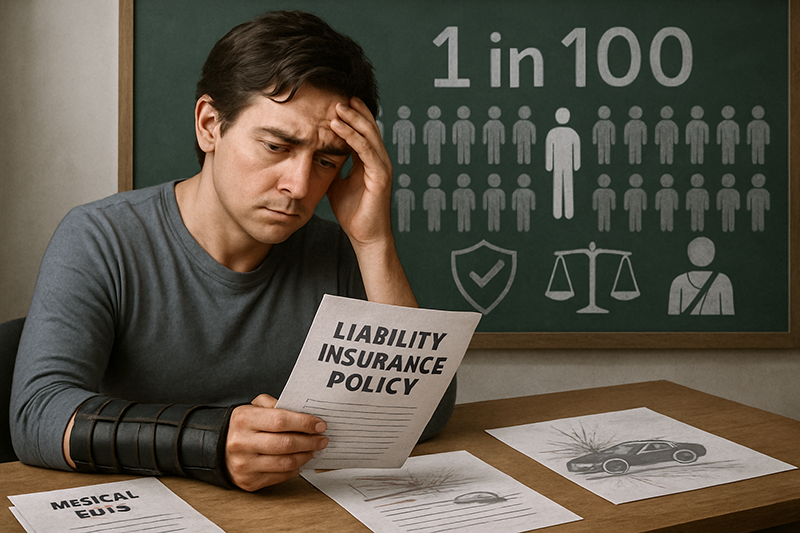

If you have been injured in an automobile accident through the carelessness of another person, you have a bodily injury claim. Nine times out of ten that bodily injury claim will be paid through the other driver’s liability policy. Of course, that means that it is of some importance that you understand what a liability insurance policy is. If you do, you are in the decided minority. As stated in the Foreword to this book, I have talked to thousands of Alaskans and thousands of people from the state of North Carolina

and it is seldom that I talk with someone who actually understands what liability insurance is. On average, only 1 in 100 people actually know what liability insurance is and what it does. Think about that.

If you want to drive a car in any state in the Union, you have to purchase liability insurance. Insurance companies sell it to you and market to you for your business but they do not feel any obligation to educate you as to what liability insurance is. They certainly do not feel that there is any advantage to doing that because the less that you know, the better it is for the insurance companies.

Liability Insurance-What is it?

Most people have liability insurance backwards. They say, “well, this person hit me, it’s his fault and he has ABC insurance. Therefore, ABC owes me for my medical bills, lost wages, pain and suffering, etc…” That statement is factually inaccurate. From a legal standpoint ABC owes the injured person in that example nothing. ABC may ultimately pay that person, but ABC does not owe that person. It is a nice distinction and it is a legal distinction, but it is an import distinction for any claimant to understand. In order to owe someone something one must have received something from that person to begin with.

It is the receipt of that thing, typically money, which creates the debt and

obligation from the recipient. In other words, and using the example above again, ABC Insurance has no duty or obligation to the claimant in a liability insurance context because they have received nothing that created an obligation on their part from the claimant. Who has given ABC Insurance something in that example? The at-fault driver. The at-fault driver paid them money in the form of premiums. It was that payment that created a duty or an obligation from ABC.

ABC says implicitly in their contract, “Pay us this amount of money and we will promise to do two things in the event that you have an accident”. There are two things that ABC promises that person, and

these are the same promises that are made to you in your liability insurance policy with whichever company you have.

1. The duty to defend. This is just what it sounds like. The liability insurance company promises that if their insured is sued in a court of civil law over the alleged negligent operation of their vehicle, the company will defend them, and by defend I mean that the company will hire a lawyer to go to court with them and answer all legal issues. The company will pay for the court reporter and depositions. The company will pay for experts that are required to testify at trial to provide an adequate defense. The company will pay for any court costs or copying and reproduction costs. In short,

the unaffordable cost of defending oneself in court is covered by the liability insurance company’s duty to defend.

2. Duty to indemnify. Indemnify is a legal word that means essentially “pay on some other person’s behalf”. In the context of a liability policy it means that the liability insurance carrier will protect their insured against a jury verdict. I’ll use the example above to explain further; if you file a lawsuit, jump through all of the evidentiary hoops, tell your story to the jury, and get a verdict for money damages against ABC’s insured, ABC will pay that verdict against their insured up to the policy limits and protection that their insured purchased.

There you have it, the long and the short of a liability insurer’s obligations-what the company owes and who they owe it to. It is important that every claimant understands exactly what that means. The one and only reason that any liability insurance carrier pays any claimant (remember there are no government threats and good faith statutes here) is because the claimant (the injured party) represents an exposure. That is, the injured person can trigger the obligations that the liability carrier has to their insured. If the injured person files a lawsuit, the company will be taxed with the cost of defending the lawsuit, and also risk the exposure of the jury trial (for

which they must pay the verdict up to the policy limits).

That’s it. The only reason that any insurance company pays under a liability policy is because the claimant represents a threat of litigation. Implicit in the fact that their insured has been accused of causing an accident is a threat that the injured person will file a lawsuit, tax them with defense costs and get a fair verdict from a jury of 12 of their neighbors. Insurance companies do not pay because the claimant seems nice or because it’s the right thing to do or because they’re the “Good Hands People” or a “Good Neighbor” or whatever. They pay because they have a risk and they have two obligations to their insured.

If you eliminate that risk, the insurance company will not pay you fairly. I cannot tell you how many times when working for insurance companies that claimants would call and shoot themselves in the foot. “I don’t like lawyers.” “You don’t have to worry about me. I’m not going to file a lawsuit.” “I don’t sue people.” “I need money now. I can’t pay the rent. I’m out of work.” I have heard all of these assertions and I can tell you that an adjuster who hears these assertions is actually hearing the claimant saying, “I don’t understand the process. I’m unrepresented and I’m not threat to trigger any obligation that you have to your insured. Please pay me whatever

you will. Please pay me whatever you think I’ll accept.”

Why do insurance companies pay?

Now, it’s important to understand why insurance companies do pay. As explained above, they will pay you but they don’t owe you. They will pay you one time and one time only and in exchange for one thing only. They do not pay as you incur medical expenses or as you miss time from work or as your mortgage payment is due. They pay only in exchange for a release- which is a binding, written promise that you sign, stating that you will not sue their insured. Once that document is signed and money has changed hands, you no longer have a

cause of action. You no longer represent an exposure or a risk to the insurance company.

So, it is of vital importance that if you do settle your case, you should receive an amount of money that is a fair guess of what you would receive from a jury of 12 of your neighbors. That is a fair settlement. The insurance company gets their peace, they avoid paying defense costs, they avoid the exposure of a huge verdict, and you get a fair and reasonable guess of what a jury would pay you without having to wait two years for your day in court. Here I’ll state for the first time that about 90% of our cases settle privately, without ever going to court.

What is my claim worth?

As stated above, your claim is really worth what a jury says. People certainly do not like to hear this but the truth is that everyone involved in your case (you, your attorney, the defense attorney, the insurance adjuster) is guessing about what 12 strangers would do with your case- twelve people that no one has laid eyes on yet would ultimately determine the value of your case. Now, those are educated guesses based upon years of experience, but they are guesses nonetheless. That’s why settling is often the best course of action for everyone involved. The cases that we have that typically do not settle are those cases where there is a dispute in liability, or

where the insurance company has asserted some doubt about whether the injuries complained of were actually caused in the accident, or, frankly, where our client has unrealistic expectations with regard to what a jury will pay for their claim. Without one of those complicating factors just about every case settles.

To discuss further what your case might be worth we should think about what a jury would hear and what a jury would be instructed when a case is tried. Keep in mind that when we discuss what a jury would do, we are doing that only to try to determine what your case might be worth. It is not a certainty or even a likelihood that a given case will need to go

to court, but at the end of the day it is the opinion of the potential jury that will drive the value of the case. Accordingly, it is important to understand what a jury would be instructed.

A jury would be instructed to award an injured person an amount of money adequate to cover all of the medical expenses incurred as a result of the defendant’s carelessness. The jury would also be instructed to award money damages to compensate the claimant for any time missed from work, as long as the jury believes that the missed time from work was caused by the injuries suffered at the hands of a defendant.

Those damages are called special damages- damages that you can write on a chalkboard. “This is how much my medical bills were.” “This is how much time I missed from work and how much I get for each day of work.” Easily computed. Where the jury is really leaned on heavily is in the computation of what are called general damages. A lot of people call these damages “pain and suffering damages”. The jury will be asked to come up with a number- an amount of money that is a fair compensation for the experience suffered by the claimant at the hands of the defendant (the physical pain, the mental anguish, the inconvenience, the financial

strain, the loss of intimacy with one’s loved ones, etc.).

As you can imagine, that number tends to outstrip the special damages. If you have recently suffered injuries in an accident, you no doubt understand the often devastating impact that these injuries have on every aspect of the injured party’s life. It is important for the jury to understand the accident’s true impact so that they can evaluate general damages. Here I should mention the importance of getting proper medical treatment. Medical treatment should consist of following the orders and advice of one or more medical professionals selected by the injured person.

Medical treatment after an accident.

It is important that the injured person take control of their medical care and get all of the care necessary- and that they also decide whom to trust. There is no reason that an injured person should follow the medical advice of a personal injury attorney or especially an insurance adjuster regarding who to see and how much treatment to get. The rules are these: if you do not need treatment, do not get treatment. If you do need treatment, get the treatment that you think is appropriate and follow through with your physician’s advice.

I cannot over-emphasize how important it is to get medical care. Medical care does a

lot of things for a claimant, all of them good. Medical care virtually assures you that you will heal more completely than you would without a doctor’s care. Medical care virtually assures that you will heal more quickly than you would without proper treatment. Medical care likely means that you will suffer less pain than you would going alone without the care of a physician. Lastly and certainly least importantly, medical care will document the problems that you are having and increase the value of your case- certainly from a settlement standpoint.

Let me take a moment to explain what I mean by that. I often take calls from individuals who will say that they were

badly injured in a car accident- that they couldn’t get off of their couch for two weeks, that they couldn’t work for three weeks, that they are still suffering problems six months after the accident. When I ask them what sort of medical care they have received, they often will reply that they only went to the emergency room and have since relied upon over-the-counter medication. Their case is likely worth very little. Setting aside the issue of whether they could have healed more quickly or completely with medical care-that is not the focus of this attorney or this book-that individual has failed to produce a written documentation of her physical injuries.

Without documentation it is very challenging to convince anyone that you have suffered serious injury. Jurors are skeptical. It would be difficult to go in front of a jury and claim serious injury without any medical treatment. However, if jurors are skeptical, insurance adjusters are categorical when it comes to the issue of little to no treatment from an injury claimant. To understand why, one must understand a little about being an insurance adjuster.

Being an insurance adjuster is not a fun job. You have several levels of management looking at everything you do, and when you settle a case the first thing that happens to the file is that it often goes to a claims auditor. The claims

auditor carefully reviews the file and asks the adjuster for justification of every item that is paid. “Where did you come up with that number?” “How do you justify paying for this?” The insurance adjuster is stuck with the cold record, as it were- the medical records of the treatment from the claimant. Even if an adjuster subjectively believes that a claimant was injured, she cannot pay that claimant money for pain and suffering absent any documentation. Doing so makes for a short walk to the unemployment line.

In short, insurance adjusters cannot pay you because they think you are a nice person and believe that you were really hurt. They have to document every dime they pay, and without medical records

they simply will not pay general damages. Now, a jury may pay for general damages if they hear you tell your story and subjectively believe that you had a hard time and that you deserve compensation for your pain and suffering, but an adjuster cannot. Since every client and claimant that I have ever met has told me that they do not want to litigate their case- that they would rather settle privately- it is important for claimants to understand that they must get proper medical care in order to document their pain and suffering to the extent that they can get a fair settlement privately from a liability insurance carrier.

That is a brief overview of liability insurance and what makes a claim valuable, but oftentimes we get a case where there is liability on the part of the other driver but no liability insurance. What happens then?